https://www.visualcapitalist.com/200-years-u-s-stock-market-sectors/)

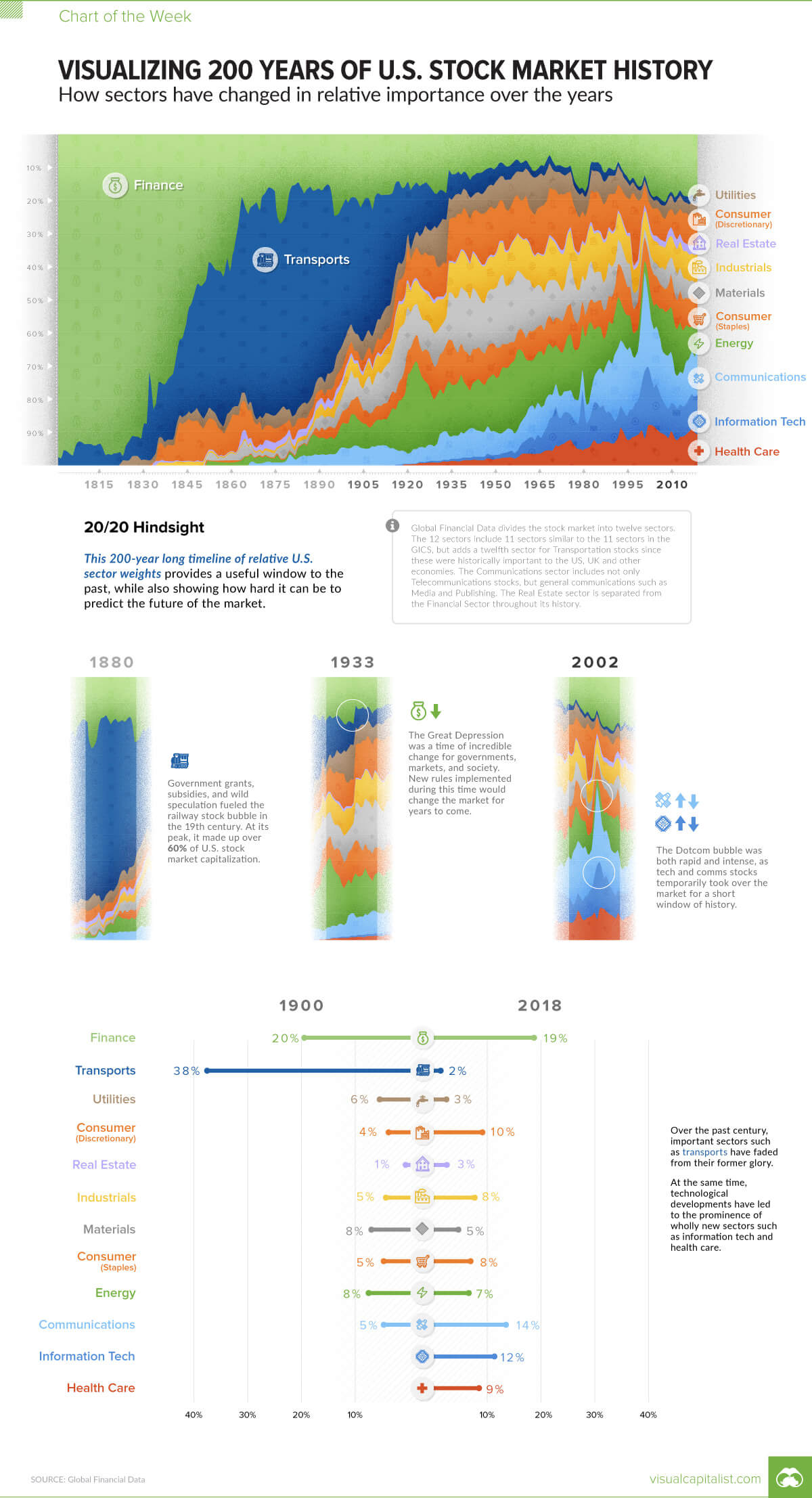

Each quarter we give our clients the chance to huddle together and receive some analysis regarding what transpired in the U.S. markets in the proceeding quarter. One of the staples we like to share is how the major asset classes performed and compare it trailing performance during recent years (like this chart below). It is always interesting to see how much fluctuation there can be in short period of time. For example, notice 2017’s leading sector of “Emerging Markets” fell completely to the bottom in performance in 2018 while “Cash” demonstrated the inverse.

Read More

What’s the secret to Col. Sanders’ recipe for fried chicken? Is the reason Coca-Cola tastes different from Pepsi based on a formula locked up in a vault at corporate headquarters? For many companies, their trade secrets – also known as intellectual property (IP) – are a key differentiator and the primary reason for their success. For some, it’s a recipe or a chemical formula. For others, it’s customer data or proprietary technology.

Read More

“Let her sleep, for when she wakes she will shake the world.”

-Napoleon Bonapart speaking about China

Car Trouble

General Motors recently announced the pending closure of three U.S. assembly plants and the discontinuation of six cars made at those plants. While large sedans are no longer big sellers in the United States, they remain popular in China, and GM will continue to manufacture them there.

Read MoreThe Tax Cuts and Jobs Act of 2017 reduced federal income tax liability for some, but not all, Americans. Wealthy residents of California, New York, and other high-tax states could face a higher tax bill when they file their 2018 return.

While cutting tax rates on ordinary income, increasing the standard deduction and doubling the federal estate and gift tax exemptions, the tax legislation also capped the deduction for state and local taxes (SALT). While once open-ended, the SALT deduction is now limited to $10,000 ($5,000 if married, filing separately).

Read More

Given a choice, which would you choose: a guaranteed fixed income for the rest of your life, or a lump sum that you could invest? As it turns out, lots of people prefer a sure thing.

This is what a recent survey showed about public sector employees posed with the option to select a defined benefit pension plan or a 401(k)-type defined contribution individual account. In fact, even when the defined contribution plan was the default option and workers had to proactively choose the defined benefit pension plan, they made the effort. In the eight states studied that offered a choice between the two options, all had employees choosing pensions at rates of 75 percent or higher in 2015.

Read More

2018 marks the 10th anniversary of the Great Recession of 2008. Despite a painfully slow recovery, U.S. economic growth has been sustainable. The stock and bond markets continue to perform well, unemployment is low and the economy is generally considered healthy and booming.

Read More

The fantasy of what retirement will look like and the reality are sometimes very different. How much you have saved versus how long you can live a particular lifestyle can sometimes fall into the category labeled “unrealistic”. Though not for lack of trying, many retirees find that the life that they had in mind for retirement does not match up perfectly with their budget based on their retirement income sources. As a result of this disparity, many still working Baby Boomers plan to continue working past the age of 65 or don’t see themselves retiring at all. A third of boomers plan to still earn a steady income during their retirement. The fact is, a majority of boomers do not have the retirement savings to support themselves without working. A paltry 15% feel they have saved enough to retire. Additionally, one-third of those nearing or in retirement have not devised a written plan or strategy for their retirement assets and income.

Part of the challenge in funding retirement is that people live a lot longer. A person who retires at 65 can be expected to live another twenty years. Someone thinking they will just continue to work at their current job, for their current pay indefinitely is, unfortunately, being unrealistic. While age discrimination is illegal, many companies find a way to push older workers out in order to establish younger professionals in leadership positions. As a result, those who were hoping to stay in their position are laid-off or demoted.

Read More

You have lived a lifetime together. You have raised children, watched them grow, experienced life’s greatest moments and, undoubtedly, some of life’s hardest moments too. This bond has made your marriage strong but despite all of this, retirement may bring a new set of challenges that you and your spouse did not anticipate. If you’re feeling frustration or isolation as you adapt to life in this new chapter you are certainly not alone. According to a recent study by the Pew Research Center, the rate of divorce among American adults over 50 has doubled since the 1990s.[i] This dramatic rise is likely due to a broad spectrum of contributing factors, but one of those may be lack of planning in advance for a shared life in retirement.

In this article, we share some key elements to success for a happy marriage in retirement.

Read More

If you are among the millions of people worried about running out of money during retirement, there are steps you can take now to improve your financial picture for an extended retirement and a long and healthy life.

According to the TransAmerica Center for Retirement Studies, longevity risk is the top retirement fear of working Americans. As life expectancy has increased while retirement savings has decreased overall, people are relying on less money for a longer period of time in retirement.[i]

Fortunately, there are many strategies, investment vehicles and practical steps that can be implemented to avoid outliving your money.

“Two roads diverged in a wood, and I—

I took the one less traveled by,

And that has made all the difference.”

–Robert Frost, excerpt from the Road Not Taken

In a recent article from Financial Advisor Magazine that identified the regrets many people have for not taking more risks in life. “Among the top regrets were: not following their dreams, not taking risks with their careers, not taking risks with their lives in general, and not being gutsy enough in the choices they made.”[i]

What was reassuring about these findings is that many people vowed to fix these regrets by taking more risks with the time they have left. There is an optimism there that is unique to our time. People are living longer, way longer than we were even a few decades ago and with that comes opportunities to evolve and edit things about our lives that don’t make sense or don’t satisfy us regardless of our age or stage in life.

Read MoreRecent Posts

Consider an Annuity Even When the Market’s Humming

Perhaps you are familiar with an annuity. The basic premise is that you convert a lump sum of money into a stream of income. Unlike an investment, once you commit a fixed amount of money to the insurance company, that company is contractually obligated to provide you a minimum level of income with the option to continue receiving it as long as you live. All guarantees are backed by the financial strength of the issuing insurance company.

Tech Trends

There are different formulas for launching highly successful companies. First, create a product that solves a problem that no one knew they had — for instance, how online search engines replaced encyclopedias. Then, there are ideas that help solve problems that plague millions of people.

Back pain, for example. Not only do approximately eight in 10 adults experience low-back pain at some point in their lifetime, but it’s also the most common cause of job-related disability.

One individual who suffered severe back pain while sitting at work all day decided to invent a new kind of desk. This desk would allow him to stand while he worked, alleviating his back pain. This man was a co-founder of VARIDESK, a new type of office furniture manufacturer. But this new company didn’t just enter the office supply industry; it introduced a new sales model that was key to its rampant success: Selling online direct to consumers.

Retirement Planning Challenges

In 1985, only 10 percent of people aged 65 and older were either in the workforce or job hunting. Today, that share has doubled, for a couple of reasons. First, fewer 65-year-olds have enough money to retire. Second, the number of people in this demographic with a college degree has more than doubled (53 percent today vs. 25 percent in 1985).

Boosting Financial Literacy is a Top Priority

Financial literacy has always been a challenge. However, now that much of the burden of retirement income has shifted to employees instead of employers, it is all the more important that we begin teaching the principles of saving and investing to people as early as possible.

Stock Buybacks Explained

When the 2017 Tax Cuts and Jobs Act reduced the corporate tax rate from 35 percent to 21 percent, the hope was companies would spend their influx of money on expansion and increased jobs and wages. Instead, public companies’ most popular way to spend the excess capital has been to buy back their own stock.